March 28, 2022—The following is a pre-publication version of a Schiller Institute policy proposal, which was researched and written by an Executive Intelligence task force of Claudio Celani, Richard Freeman, Paul Gallagher, Marcia Merry-Baker, Dennis Small and Karel Vereycken.

I. Summary of the action plan

The developments of 2022 to date have made it abundantly clear that Lyndon LaRouche’s forecasts over the last half-century, about the unavoidable breakdown crisis of the post-Bretton Woods floating exchange-rate financial system, were shockingly accurate. World production of physical economic essentials is plummeting; hyperinflation of financial aggregates has unleashed soaring prices of consumer and producer goods, making them unattainable for a good part of mankind; trade warfare under the guise of sanctions has erupted worldwide; and pandemics of old and new diseases have already taken the lives, directly and indirectly, of some 18 million people. World famine is impending.

Political leaders and the mass media in the West pathetically blame Vladimir Putin for all of this—and more. But the actual, underlying cause is the decades-long plunge in the “potential relative population density” of Mankind as a whole – LaRouche’s metric of the power of a society to reproduce itself at ever-rising levels of well-being, science, and classical culture for a growing population – a collapse which is the result of the austerity policies imposed over a half century by the City of London and Wall Street.

The mechanism through which this policy is being carried to its “final solution” today is a radical decoupling of the world economy into two bitterly antagonistic blocs—a militarized NATO-dollar bloc, and the Belt and Road bloc—both of which are meant to be plunged into an inferno of depopulation and war, very possibly including thermonuclear war.

It is particularly telling and terrible that what had been the burgeoning Belt and Road rail links extending from China, through Russia, and into Europe have been almost totally disrupted by the ongoing sanctions and war.

It is now time for Lyndon LaRouche’s programmatic solution to this crisis to also become abundantly clear, and acted upon, across the planet — while there is still time to do so. Against London’s Malthusian decoupling of the world’s physical economy, the nations of the world must instead be recoupled around a program of economic growth and security for each and all, a new international architecture of security and development.

The essentials of that programmatic policy were laid out by LaRouche in his 2014 Four New Laws, which are as applicable today as when they were first designed eight years ago (see Box 1 at the end of the document). Under today’s circumstances of overt “total war” being waged by the financial Establishment against Russia (and soon China), which leads to the same results, in effect, as strategic carpet bombing of enemy territory, an immediate Action Plan centered on those Four Laws is required:

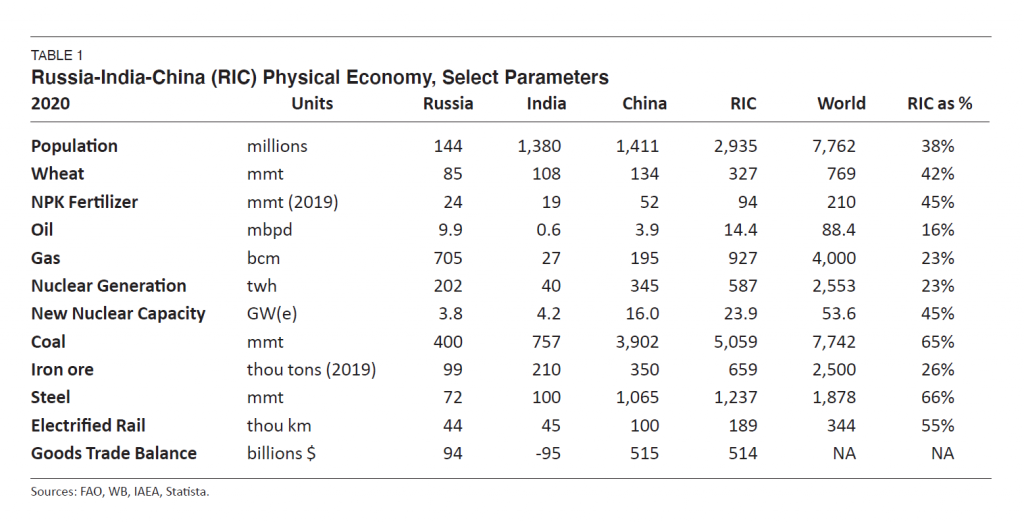

- Physical economy: Russia has already adopted war-economy measures to defend its basic national capacity and guarantee self-sufficiency in key economic essentials. However, the “Strategic Triangle” of Russia, India and China will be even more effective at meeting the essential physical-economic needs of their combined population, which is 38% of the world total, if they work together. That RIC combination – which was the original core of what later became the BRICS – produces 43% of the world’s wheat, 23% of its natural gas, 66% of its steel, and prodigious quantities of critical minerals. It also has world class capabilities in nuclear energy, rail and other infrastructure construction, space science, and other advanced technologies (see Table 1).

Table 1

Despite shortcomings in certain economic sectors (machine tools and other capital goods, pharmaceuticals, aircraft, etc.) the RICs are strongly positioned, in terms of physical economy, to establish a “regional bloc which operates either outside, or in parallel to the existing IMF system,” as Lyndon LaRouche recommended years ago. The alliance of China’s Belt and Road Initiative (BRI) and the Russia-led Eurasian Economic Union (EAEU) is already an operational cornerstone of such a proposed new arrangement.

- Fixed exchange rate system: Trade and productive investment within such a bloc will occur by establishing a fixed-exchange-rate relationship among their currencies, with a small currency band for temporary fluctuations. This arrangement will wall out any penetration by speculative dollar-denominated or related financial flows. Thus, the parities among their respective currencies will have no relationship any longer with the speculative floating-rate dollar system, but will be directly established by government-to-government agreements, and not by the rigged speculative “market.”

A regional common currency will also be negotiated to facilitate international trade, investment, and settlement of accounts – with a gold-backed renminbi being one leading option. This will permit the “negotiation of a nested array of long-term sets of protectionist treaty-agreements on credit, tariffs, and trade among a set of leading nations,” as LaRouche wrote in 2004 (see Box 2 at the end of the document).

- Full-set capital and exchange controls, and directed credit: Each of the countries will also establish a totally protected national currency and banking system, requiring: full-set capital and exchange controls; a fixed exchange rate vis-a-vis other currencies (as indicated in point #2 above); and the issuance of directed, productive credit at low interest rates to priority projects. In the case of Russia, a gold-backed ruble (or new “heavy ruble”) would meet those requirements in an exemplary way; gold-backed currencies could well be put in place in China and India as well, and this could be extended to the common currency.

The era of high interest rates to attract “carry-trade” speculative financial flows from abroad will be brought to a screeching halt. In a developing sector nation, such a strict separation between the protected production-based national currency, and the speculative London-directed international dollar, performs the same function that Glass-Steagall banking separation does in the United States. This is a prerequisite for establishing a Hamiltonian National Bank to organize the issuance of new, low-interest productive credit flows into high-technology sectors of the nation’s physical economy – “a massive supplement of long-term credit for capital formation, with initial emphasis on capital formation in basic economic infrastructure,” in LaRouche’s words.

- RIC+: The RIC nations will serve as the initiating core of a new international architecture, which will be open to all nations willing to participate on the basis of such sound physical-economic principles. There is little doubt that most nations in the developing sector will find this new architecture far more beneficial to their own needs than the devastation now being imposed on them by the bankrupt trans-Atlantic financial system, and will quickly orient to such an effort. One possible immediate building bloc is the Shanghai Cooperation Organization or SCO (Kazakhstan, Kyrgyzstan, Pakistan, Tajikistan, and Uzbekistan, in addition to Russia, India and China), which some leading experts have suggested as sufficiently broad to function as an option to initiate a new gold-backed non-dollar monetary system, based on a treaty agreement among the initiating nations.

The massive export of capital goods to developing sector nations will be central to the productive expansion of the RIC bloc. Major infrastructure projects in these nations will also be an integral part of the world economic recovery. Long-term, low-interest credit for such activities will be issued in the new RIC common currency, in much the same way that the renminbi is already being used by the BRI today, only on a much broader scale. Credit created for advanced-technology productive economic activities – as distinct from speculative ones – is not inflationary, and is readily repaid out of the increase of productivity which such investment will induce.

- The U.S. and Europe must join the Belt and Road: It will be of special importance to bring the United States itself, as well as the nations of Europe, into this new set of international agreements. The American and European people and their economies will do far better in association with the RIC and the Belt and Road Initiative, than under the de-industrialization and depopulation regimen that they are now facing under the current bankrupt British-run system. Lyndon LaRouche referred to this policy as a Four Power alliance (Russia, India, China, and the United States) which alone would have the requisite power to put an end to the British Empire once and for all. Doing so only requires that the U.S. return to its founding Constitutional purpose, including the American System of economy pioneered by Alexander Hamilton, and that sovereign nations of Europe act similarly.

- Reconstruct Ukraine Through East-West Cooperation: The immediate focus of such economic cooperation for the benefit of all, will be Ukraine. What is today a bloody battlefield will become a model of East-West cooperation. The once-powerful Ukrainian economy – destroyed by 20 years of economic liberalism after independence; followed by another ratchet down after the 2014 Western-led Maidan coup d’etat; and now being ravaged by war – can be reconstructed and revived by cooperative efforts. Ukraine will become the hub of Belt and Road transit from China to all of Europe, rebuilding Ukraine’s once-powerful scientific, heavy industrial and agricultural sectors for the benefit of the world.

The above six measures are not a long-term strategy; they are not a medium-term proposal. They are a short-term action plan required to stop the massive economic destruction that is already underway, stop the geopolitics-driven wars, and provide the necessary architecture for accelerated growth and development of all nations.

II. Sanctions Are Decoupling the World Economy into Oblivion

The physical economy of the trans-Atlantic sector has been in accelerating decline for approximately the last half-century, ever since Nixon’s August 1971 announcement of the end of gold backing for the dollar and the introduction of a speculative floating-exchange-rate system in its place. Then, in early 2020, the COVID pandemic caused a further sharp ratchet downward, exposing a global real unemployment rate of 46%, which had been covered up with “informal employment” which only condemned hundreds of millions of people to perennial poverty and hunger. In November 2021, the Glasgow COP26 circus launched a drive to impose a medieval policy of further deindustrialization, under the guise of the Great Green Reset to combat “climate change,” which is taking the physical economy down even more, hitting the energy sector particularly hard.

And now we have the macabre sanctions policy against Russia and China, which went into high gear in late February 2022, plunging the planet’s physical economy down to levels of potential relative population density which inexorably will mean the reduction of the world’s population by billions, unless reversed. It must be emphasized that the ongoing collapse of the world’s physical economy was not caused by the current crisis around Ukraine – it pre-dates it by decades. But the sanctions regime is meant to be the coup de grace to Mankind as we know it.

A) Food and Agro Emergency

Start with food – where the consequences of the sanctions policy are hitting the developing sector with a particular vengeance. Liu Zhiqun, a noted Chinese economist at the Chongyang Institute for Financial Studies, put it succinctly in an interview with CGTN’s Tian Wei on March 23. Asked to comment on the global economic effects of the U.S. sanctions regime on Russia, Liu stated: “It has already been estimated that the spread of COVID will lead to conditions of starvation for 200 million people. But with the effects of the sanctions regime, that number will be 1 billion.”

There was already a grave under-production of food as of two years ago, before the 2020 pandemic and 2021 hyperinflation had set in, such that in 2019 over 810 million people lacked sufficient food, and famine was worsening. As of 2021 year-end, the World Food Program estimated over 230 million were nearing famine, and agriculture production was in turmoil from farm input shortages and high prices.

The shock of the sanctions on top of this is devastating. Russia, along with Belarus, has been a major source of the baseline NPK—nitrogen, phosphorous, potassium—fertilizers for the world, which is now cut off. Yields will plunge of wheat, corn, and rice—the three staple world grains — along with reduced area planted. Until now, Europe got 25% of its basic NPK from Russia, directly or indirectly. Brazil and other major producers are scrambling. Svein Tore Holsether, the President of Yara International, one of the world’s largest fertilizer companies, summarized in March: “Half the world’s population gets food as a result of fertilizer…and if that’s removed from the field for some crops, [the yield] will drop by 50%.”

The stoppage of grain and other commodities, as well as fertilizers, from the Ukraine-Belarus-Russia agriculture zone is an immediate world-scale emergency. Russia and Ukraine together are the largest wheat exporters in the world, accounting for a third of the 200+ million metric tons of wheat traded yearly. This especially hits the wheat import-dependent nations of MENA (Middle East-North Africa) region, many of which were 70% or more dependent on Ukraine and Russia. Many European nations had come to be reliant on Ukraine for feed grains (barley, corn, etc.) which are now cut off. Ukraine has accounted for 19% of the world’s annual corn exports. The World Food Program had obtained half of its grain from Ukraine in recent years. Ukraine and Russia together also accounted for 75% of the sunflower seed oil traded internationally, a significant part of world edible oils exports.

In lockstep with the shortages, the price of food has been soaring, placing the reduced amounts produced out of reach for millions. According to the UN Food and Agriculture World Food Price Index, food prices rose 54% in the year and a half from May 2020 through February 2022.

Besides the immediate food impact, seeds, crop protection chemicals and other farm inputs for the 2022-2023 crop cycle are all in jeopardy. Two of the world’s largest seed suppliers, Bayer AG and Cargill Inc., have threatened Russia with a cut off of wheat seeds for 2023, in line with the U.S. sanctions policy.

There are five areas of urgently needed response.

- National governments must exert their sovereign responsibilities to confer internationally and direct scarce food stocks to where they will save lives, and likewise, direct scarce agriculture inputs—seeds, fertilizer, crop chemicals, fuel–to the farm belts that can produce the maximum output in the short term. When necessary, this means overriding autonomous decisions by food and agro-cartels.

- National governments must implement support measures for independent, family-scale farm operations, and corresponding food processing operations, everywhere, according to each nation’s plans. This mode should include parity pricing, credit, and infrastructure, and will mean ending the reign of the cartel system, which has fostered export-source regions and monoculture, while millions go hungry and starve.

- The goal is doubling world food production, to end hunger. At the metric of a half ton of grain per person produced yearly (for direct and indirect consumption, through animal proteins), the world harvest should be in the range of 4 billion mt, but it is barely 2.7 billion mt, or two-thirds what is required.

- Cancel the Green Reset framework and its ideology of cutting human activity, in the name of saving the planet. In particular, stop the “30 by 30” plans in 60 nations, including the United States, which seek to take 30% of their land and water out of agriculture or other economic use by 2030.

- Ukraine, come the peace, is a world asset for high-productivity agriculture, as we detail below. Having a total of 41.5 mil hectares of agricultural land, which is 70% of the country’s total area, it ranks second in Europe after Russia in farmland area. Ukraine has 32 million ha (hectares) considered arable out of its total farmland. Nearly all of its soils are good, and half are the very fertile chernozem—the Black Earth. Rivers and Black Sea access to ocean trade are major transportation assets. The climate favors agriculture. With a reconstruction and growth plan by development specialists, Ukraine ranks not only as a productive centerpiece geographically in Eurasia, but as a bridge to a future of plentiful food for all.

B) Pulling the Plug on Europe’s Energy

The sign of a healthy economy is technologically-induced rising energy flux density in the production process, combined with increasing overall energy consumption per capita and per square kilometer. But the world energy picture has been moving in the opposite direction for decades; and the sanctions policy is ensuring that collapse will now occur at breakneck speed.

Europe’s nations and people, in particular, are lambs being led to the slaughter. In 2020, about 40% of Europe’s total energy consumption came from imported oil. In the year ending in October 2021, Russia supplied about 25% of all oil imported by the European Union. So, if you stop those oil imports from Russia, Europe takes a 10% hit in its total energy consumption. A similar situation applies to natural gas.

The situation for Germany is particularly grave.

Table 2

Germany Energy Consumption 2020

| (thousand PJ) | % | |

| Total | 12.41 | |

| — Oil | 3.97 | 32% |

| – Imports | 3.89 | 98% |

| * From Russia | 1.32 | 34% |

| — Natural Gas | 3.14 | 25% |

| – Imports | 2.98 | 95% |

| * From Russia | 1.64 | 55% |

| Total From Russia | 2.96 | 24% |

Without Russian natural gas and oil, Germany will have 24% less energy than it has today. It is highly unlikely that these supplies could be readily replaced by other sources, and certainly not quickly.

Major European governments, particularly Germany’s, fear telling their people that Russia’s (so far unsanctioned) energy exports to Europe are banned. But they are banned, in effect, by intimidation of any company that thinks of buying Russian petrochemicals, not to mention the extreme difficulty in obtaining financing and insurance for such transactions. The same is true for metals and fertilizers; Russia is a huge exporter of both. It is possible, even likely, that

by later this spring all Russian exports of natural gas, oil, and fertilizers to Europe and the United States will have stopped, even if a peace agreement in Ukraine were to have been reached. The near-total disruption of the Belt and Road corridor running from China through Russia to Europe is part of the same picture.

Russia is the third-largest oil producer in the world, and the #1 oil exporter. It produced about 11.3 million barrels per day (bpd) in 2021, of which some 7.2 million bpd were exported. Of these exports, 1.6 million bpd went to China, making it the single largest purchaser of Russian crude. Russia is well-positioned to significantly redirect its oil exports currently going to Europe (about 2.3 million bpd), to China and India, which currently imports 85% of its 4.3 million bpd requirements, but less than 3% of that comes from Russia.

Russia also possesses the world’s largest natural gas reserves, by far, with 47.8 trillion cubic meters (tcm), nearly a quarter of the world total of 205.6 tcm. In 2021, Russia produced a record 763 billion cubic meters (bcm) of gas, of which 185 bcm (24%) were exported. The two largest purchasers of Russian gas are Germany (43 bcm) and Italy (29 bcm). China only purchased some 9 bcm of Russian gas in 2020, but the two countries plan to increase those purchases up to 38 bcm in 2025, and possibly more thereafter.

Energy prices are also soaring, as part of the global hyper-inflation unleashed by the global speculative bubble of financial assets. West Texas Intermediate oil was trading at $112 per barrel on March 21, 2022, as compared to $68 per barrel three months earlier, on Dec. 20, 2021 – a 65% increase. During the same period, natural gas prices in Europe leapt from $2,190 per thousand cubic meters to nearly $4,000 per thousand cubic meters – an 85% jump. And the price of thermal coal to produce electricity more than tripled to reach an all-time high of $460 per ton on March 7, as against $134 per ton on Dec. 21. These and related commodity prices are expected to continue to soar in the months ahead.

C) Minerals and Metals

The sanctions policy against Russia will be particularly devastating for Western nations’ access to vital minerals and metals. Russia, China, and fellow SCO member-nation Kazakhstan combined produce the vast majority of the world’s essential minerals. Of the 42 most critical minerals and mineral products in the world, these three countries combined produce from 30% up to 90% of the world total, according to the authoritative U.S. Geological Survey. These minerals range from the most elementary (such as bauxite, graphite, lead, and copper), to those needed for advanced processes and microchip making, such as the rare earths, titanium, silicon, and gallium (which is used for electronic circuits, semiconductors, and light-emitting diodes), to those needed for agriculture, such as nitrogen ammonia and phosphate rock.

For 16 of those top 42 minerals, Russia, Kazakhstan and China account for more than 70% of total world production. In 2021 they produced 84% of the world’s mined production of vanadium (an alloy which makes steel shock resistant and vibration resistant, and is also employed in armor plate); 85% of the graphite; 86% of bismuth; 87% of tungsten; 87% of mercury; 91% of asbestos, and 98% of gallium (which is essential in most high-tech fields).

The three nations mine and/or produce 37% of the world’s nitrogen ammonia, which is used in fertilizers and herbicides; 45% of the world’s phosphate rock, which is used in manufacturing phosphate fertilizer; and 33% of the world’s potash, which is used in manufacturing fertilizer.

In addition to agriculture, another sector that this hits directly is automobile production. An article in the March 7 Globe and Mail noted that “the industry is also facing scarcity and price increases of raw materials from Ukraine and Russia, such as neon gas, palladium and nickel, which are all used for various purposes in automotive manufacturing.”

D) Sanctioning Scientific Excellence

Space: President Biden’s sanctions against Russia’s space program will also affect many space projects in numerous other countries, including those implementing the sanctions. For example, the decision of the European Space Agency to suspend cooperation with Russia on the ExoMars mission, initially planned to be launched late September 2022 from Russia’s Baikonur Cosmodrome in Kazakhstan, is a self-inflicted disaster.

A plan without Russia for ExoMars will involve more than replacing the Russian-built Proton rocket. Russia also built a landing platform called Kazachok that will have to be replaced. The rover itself includes Russian instruments and radioisotope heating units supplied by Russia. ESA’s statement also addressed Russia’s Feb. 26, 2022 decision to halt Soyuz launches from the EU’s launch site at Kourou, French Guiana and withdraw its personnel there in response to the European sanctions. That decision puts five European missions in limbo—two launches of Galileo navigation satellites, ESA’s Euclid space observatory and EarthCARE Earth science satellites, and a French military reconnaissance satellite.

It is a bitter irony that the attack on Russia’s space science is also a body blow to Ukraine’s space capabilities. Since 1991, the US, Europe and Russia have cooperated in Ukraine, since the latter has been a major player in the world’s space industry since the 1950s. It is not often reported, but Ukraine is a top designer and manufacturer of space launch vehicles (including Russian) rocket engines, spacecraft, and electronic components. Ukraine’s Zenit rocket is even Elon Musk’s favorite. With 16,000 employees, the Ukrainian Space Agency nearly matches NASA’s size. A legacy institution from the Soviet era, the agency controls 20 state-run corporations centered in Ukraine’s space cluster, a region between the cities of Dnipro, Kharkiv and Kyiv.

Nuclear: Nuclear energy is another Russian (and Ukrainian) high-tech capability that is being targeted by the sanctions. Russia is the fourth largest nuclear energy producer in the world at 202 twh, after the U.S., China, and France. But it is a world leader, along with China, in new nuclear plants under construction both inside the country and abroad.

Currently, Russia operates 38 nuclear power reactors inside the country; another 27 are planned; and a further 21 reactor units are proposed. Rosatom, Russia’s state-owned State Nuclear Energy Corporation, has stated its goal that Russia will derive 70% of its electricity from nuclear reactors by the end of the twenty-first century.

Outside of Russia, there is an aggressive building regime. Russia has either already built, is building, or will be building nuclear reactor-units in the following countries: Armenia (1); Bangladesh (2); Bulgaria (2); Belarus (2); China (8); Egypt (4); Finland (1); Hungary (4); India (4); Iran (3); Slovakia (4); Ukraine (15); Uzbekistan (1). In Bolivia, Russia is establishing a nuclear science-led science city, which will have a research reactor facility.

Russia is particularly intent on bringing nuclear power to Africa. President Putin stated at a 2018 BRICS summit in Johannesburg, South Africa: “I would especially like to note that Russia is planning to step up its assistance in development of national energy in African states. In the nuclear power industry… we offer our African partners the creation of an entire industry on a turnkey basis. Agreements on cooperation in the field of atoms for peace have been signed with a number of countries in the region, while in some of them the work has acquired a practical dimension. All these projects will be of strategic importance for Africa, where, according to different estimates, as many as 600 million people still live without electricity.”

Medicine: In August 2020, Russia became the first country to announce the development of a COVID-19 vaccine, the two-shot Sputnik V, and a while later, the one-shot Sputnik Light. There was an all-out British effort to make sure that the Sputnik vaccines were not approved. The West derided the Sputnik vaccine until February 2021 when the Lancet medical journal published its findings that the Sputnik V had a 91.6% efficiency rate in a study with 20,000 participants.

British and America sanctions even before the war with Ukraine sand-bagged the process. On March 1, 2021, the United Kingdom imposed sanctions against the Russian Direct Investment Fund (RDIF) and its head Kirill Dmitriev. The United States followed suit. The RDIF worked with the Gamaleya Research Institute of Epidemiology and Microbiology, which developed the Sputnik V vaccine, to organize the production of Sputnik V and promote it in foreign markets.

III. Sanctions Are Accelerating the Trans-Atlantic Financial Breakdown

Before February 25-27 (the dates of the Russian invasion of Ukraine and the launching by NATO nations of the “nuclear option” sanctions) the U.S. inflation rates had already surged from 1.5% to 6.9% for the official consumer price index and to 9.8% for the official producer price index. The EU inflation rate had surged from about 1% to 4.8% for the official consumer price index and to 16% for the official producer price index.

So, when the big inflationary “sanction shock” hit all commodities from March 4 on, and the availability of crucial food, energy and mineral commodities began to be cut off, the trans-Atlantic financial system had already been on fire with inflation created by the effort of the major central banks to preserve the biggest private banks and fortify them against the coming collapse of the debt and related derivatives bubble – an effort doomed to failure.

In one of the biggest fields for the spread of that fire, the U.S. housing market, notorious in the 2007-08 global crash, the roaring inflation cannot be attributed to any effects of the war in Ukraine or NATO’s economic warfare against Russia. But this market is inflating toward another collapse and alarming officials of the Federal Reserve. The average U.S. monthly mortgage payment in mid-March was higher than one year earlier by a shocking 28%, according to the U.S. National Association of Realtors. Home sales are dropping steadily since the Fall of 2021, as homes are becoming unavailable and unaffordable for most households. And average rents across the country are reported up 14.9% in a year.

Regarding energy prices in Europe, this roaring inflation created by central bank money-printing and derivatives speculation had already doubled and tripled energy prices well before the war.

The biggest central bank, the Federal Reserve, is now clearly worried about having lost control of what one of its governors. Christopher Waller, on March 19 called “raging inflation”. Three governors or regional presidents – Rafael Bostic of Atlanta, Georgia; James Bullard of St. Louis; and Waller – are calling for multiple rate increases of 0.5% in each of the Federal Reserve’s next few meetings, panicked because their current planned increases have no chance of slowing the inflation. This tightening policy will fail as miserably as the opposite quantitative easing approach did – because the underlying speculative bubble of quadrillions of dollars is unpayable under any scenario.

With this prelude, the hyperinflationary shock which propagated from the week of Monday, March 7 blew most of the liquidity out of the sphere of producing, distributing, and trading the many commodities indicated above. A payments crisis exists among many thousands of companies in these sectors, and clearly affects their banks. No less a bank than JPMorgan Chase, the biggest in the United States, was expressing in the following week, through its global commodities chief, great anxiety about the bank’s exposure as a counterparty to all these firms. Lending in these sectors has effectively stopped. Bloomberg News headlined on March 18, “The World’s Biggest Commodities Markets Are Starting to Seize Up.” The European Federation of [the world’s largest] Energy Traders on March 16 asked the central banks to provide “time-limited emergency liquidity support to ensure that wholesale gas and power markets continued to function”.

Shortages of vital commodities are everywhere and those caused by the NATO attempt to crush Russia’s economy are cross-feeding with those, such as fertilizers, which were already spreading because of raging inflation before February 25. Those commodities in greatest shortage are hyperinflating in price.

The phenomenon of “self-sanctioning” by large numbers of companies in Europe, North America and Oceania of Russian energy products which are not under any government sanctions, has made that term into a meme. Bank commodities traders estimate Russian oil exports to Europe are actually down by 1.5 million barrels per day (bpd) despite being unsanctioned, for example. Total Russian oil exports worldwide are reported to be down 2 million bpd. The IEA says it will be 3 million bpd over the course of 2022.

Already on March 7, Credit Suisse analyst Zoltan Poszar described well the financial shock provoked by commodities. “When the West sanctions the single largest commodity producer of the world, which sells virtually everything”, he wrote, the following is going to happen: non-Russian commodities are getting more expensive because of the new scarcity; traders need to borrow more but is there enough collateral around? Nevertheless, we are going to see a pattern of margin calls on those who went long on non-Russian commodities and short on the related futures.

“We are seeing at the 50 -year anniversary of the 1973 OPEC supply shock is something similar but substantially worse – the 2022 Russia supply shock, which isn’t driven by the supplier but the consumer.”

A default on Russian debt is also being deliberately provoked by its western creditors, by freezing (i.e., stealing) some $300 billion of their $640 billion in foreign reserves. A default will unleash margin calls on credit default swaps, whose price has increased so much that they are no longer usable by Russia’s creditors. Moscow has so far been able to service that debt, as it demonstrated by paying $117 million due March 16 and $66 million March 21 out of the frozen reserves – a procedure permitted by a U.S. Treasury Department loophole in its sanctions, which expires at the end of May 2022.

That loophole was left in place by the Treasury to allow international bondholders to safely depart the Russian market by selling their heavily discounted Russian bonds to Goldman Sachs and others, who in turn are selling such “distressed debt” to vulture funds. Those funds will then turn around and use their substantial financial, legal, and political firepower to try to force Russia to pay full face value on the bonds, which the vulture funds had picked up for a nickel on the dollar – as they did in their war against Argentina two decades back.

Foreign debt of Russian corporations is a $75 billion question mark. Such bonds have already been repriced by the market at a 70% haircut; i.e., with a loss of about $50 billion. Wall Street on Parade wrote March 7: “The Big Question on Wall Street Is Which Banks Owe $41 Billion on Credit Default Swaps on Russia.”

“There is a known $41 billion in Credit Default Swaps (CDS) on Russian debt,” the well-known financial column reported. “There are likely many billions more in unknown amounts. There are also billions more in Credit Default Swaps on state-owned Russian corporate debt and non-state-owned Russian corporate debt.”

“You have the makings of a replay of the 2008 banking crisis,” Wall Street on Parade wrote, “when banks backed away from lending to each other because they didn’t know who would fall next from toxic subprime exposure. That led to a liquidity crisis and the unprecedented involvement of the Federal Reserve secretly pumping trillions of dollars into the megabanks on Wall Street and their foreign derivative counterparties.“

On March 11, the Financial Times published the list of the most exposed western banks, using data from the Bank for International Settlements. Total exposure is given at $121 billion, with the largest chunk being in the hands of European banks with $84 billion, with Societe Generale on top of the list ($21 billion), followed by Paribas ($3 billion), Credit Suisse ($1.7 billion), Deutsche Bank ($1.5 billion). Among US banks, Citibank is the most exposed with $10 billion.

IV. Draft Plan to Reconstruct and Develop Ukraine

Peace through development is the watchword of the policy for a new security and development architecture, and it must be applied most immediately to the post-war reconstruction of a neutral Ukraine.

Although the depth of destruction as a result of the ongoing war is unknown at this time, the fact remains that Ukraine’s economy can and should be reconstructed and transformed into a leading scientifically-technologically advanced economy, as a hub between the eastern and western portions of Eurasia. It can raise its living standards and its labor force’s cognitive-creative powers, while rejecting the City of London-IMF’s destructive advice that has led it to three decades of economic devastation. It can rebuild out of the rubble which the current war is leaving int its wake.

Ukraine’s inherent potential is great. It has historically had a skilled and productive labor force with world-class capabilities in a number of areas. It has a significant industrial belt in the region between and inclusive of the Dnipropetrovsk Region and the Donetsk People’s Republic (previously the Donetsk Region of Ukraine), which has produced more than one-third of Ukraine’s total industrial output. (For the purposes of this study, we consider the disputed Donetsk People’s Republic [DPR] and Lugansk People’s Republic [LPR], whose exact status will emerge from peace negotiations, and Ukraine as part of the combined region to be developed.) Ukraine has the Yuzhmash and Yuzhnoye design and machine-building plants, involved in producing spacecraft, rockets, and forgings; and Antonov Aeronautics, which specializes in cargo aircraft, all of which could be expanded to produce space-related vehicles, but a portion of which could be retooled into manufacturing such things as laser machine tools.

Its land is endowed with 20% of the planet’s “black earth” to produce abundant wheat, grains, and many agricultural crops, for itself and export around the world. Its rail grid is aged, and in some places run down, but it could be upgraded to include electrified high-speed rail or magnetic levitation, using its privileged pivotal geographical location, to speedily transport goods and people north-south, and east-west through the heart of Eurasia, a central link in the Belt and Road Initiative. Ukraine is in fact the perfect pivot for replacing the current global paradigm of economic collapse and war, with a new security and development architecture, one based on the concept of peace through development.

Thirty Years of Destruction

Upon the 1991 dissolution of the Soviet Union, Ukraine declared itself independent on August 24, 1991, but its “independence” was short-lived. Immediately, a swarm of economists from the precincts of the IMF, Wall Street and the City of London swept in, and enforced policies of privatization, shutting down factories, firing workers, etc. Dr. Natalia Vitrenko, chairman of the Progressive Socialist Party of Ukraine (PSPU), dissected the results of that destructive policy at an April 13-14, 2013 conference, whose speech was reprinted in the May 3, 2013 issue of EIR magazine. Vitrenko reported: “Whereas Ukraine used to have 16 major machine-tool plants, which produced 37,000 machine tools in 1990, now there are only three left, which barely are on their feet; they produce just 40 machine tools a year.”

Vitrenko further noted that, comparing the levels of 2012 to 1990, after 22 years Ukraine’s electricity production had fallen 35%; its rolled steel production had dropped 57%; and its tractor production had collapsed by 94.3%. During these years of monetarist “independence,” Ukraine lost 12 million jobs, and the people got progressively poorer.

A nodal point in Ukraine’s history occurred in late 2013: Ukrainian President Victor Yanukovych decided to not sign a free-trade Association Agreement with the European Union on Nov. 21, and he looked to other alternatives for Ukraine’s development. On Dec. 3-6, Yanukovych made a state visit to Beijing. There he met with Chinese President Xi Jinping, and committed Ukraine to join the Belt and Road Initiative, whose creation Xi had announced only three months earlier in September. On Dec. 5, the Chinese Foreign Ministry commented on the meeting: “Ukraine once made important communications between the Eastern and Western civilizations, and is located on the way that the Eurasia Continental Bridge must pass. Ukraine is ready to join in the building of the ‘Silk Road Economic Belt.’ The Chinese side expresses welcome for this and is ready to discuss relevant cooperation with the Ukraine side.”

China and Ukraine signed a Strategic Partnership Agreement, and China agreed to invest $8 billion in Ukraine’s economy, according to the Dec. 6, 2013 Ukraine Monitor.

Cooperation with Russia was also on the agenda. Then Russian Deputy Prime Minister Dmitri Rogozin had formed a working group on Russian-Ukrainian industrial cooperation, involving military and joint space production, which was consolidated with Rogozin’s Dec. 1-3 tour of industrial plants in the Dnieper Bend industrial region, culminating with a meeting with Ukraine’s then Prime Minister Mykola Azarov.

These development prospects were more than the horrified British and American Establishment could tolerate, and they went “live” with long-standing capabilities in Ukraine, including Victoria Nuland, then U.S. Assistant Secretary of State for European and Eurasian Affairs, and the networks of followers of pro-Nazi collaborator Stepan Bandera, who deployed to escalate violence and chaos to overthrow the Yanukovych government — which they succeeded in doing on February 24, 2014. The pre-selected Arseniy Yatsenyuk was installed as Prime Minister on Feb. 27, 2014, at Victoria Nuland’s insistence, in order to reinstate the City of London-IMF policy that had instigated so much destruction and suffering in Ukraine for 21 years.

The continuing degradation of Ukraine’s labor force starkly exemplifies the process, as shown by the following table.

Table 3

Ukraine’s Labor Force

| Year | Total Labor Force | Agriculture | Industry | Manufacturing |

| (thousands) | ||||

| 2012 | 20,354 | 3,496 | 3,346 | 2,322 |

| 2013 | 20,404 | 3,578 | 3,275 | 2,276 |

| 2014 | 18,073 | 3,091 | 2,898 | 2,022 |

| 2015 | 16,443 | 2,870 | 2,574 | 1,839 |

| 2016 | 16,277 | 2,867 | 2,495 | 1,792 |

| 2017 | 16,156 | 2,861 | 2,441 | 1,775 |

| 2018 | 16,361 | 2,938 | 2,426 | 1,786 |

| 2019 | 16,578 | 3,010 | 2,262 | 1,833 |

Between 2012 and 2019, Ukraine’s total labor force dropped 3.96 million workers, or by 18.6%; its agricultural labor force shrank by 486,000 workers (by 13.9%); its industrial labor force fell by 884,000 workers (by 26.4%); and its manufacturing labor force (part of industrial workers) fell by 443,000 workers (by 19.5%).

In 1992, Ukraine had a total population of 51.9 million people. By 2012, it had plunged to an official 45.4 million, though economist Vitrenko said that the actual figure then was 39 million. By 2020, the official population figure was 41.4 million, including the Donbass population (though using Vitrenko’s adjustment, it would be closer to 35 million). By official standards, Ukraine has had the greatest population shrinkage of any European country between 1992 and 2020, and all of this occurred before the Feb 24, 2022 Russian military operation in Ukraine. Now, there are about an additional 4 million Ukrainians who have emigrated abroad, and an unknown number who have been internally displaced.

Reversing the Process, Reconstructing Ukraine

Ukraine can take some critical steps as part of a new international economic architecture, as presented earlier in this document.

First, Ukraine should put the greatest emphasis on rebuilding and developing its productive labor force. In a Dec. 7, 2012 webcast, economist Lyndon LaRouche said,

“We have a population of the planet, and we need every damned individual on this planet: We need ’em! They have a purpose in existing, because they can become more productive, and as they become more productive, then their children become more productive, and so forth; mankind’s ability to cope with these problems increases.”

Over approximately the next decade, Ukraine should target bringing 10 million workers back into the labor force, including 4 million more industrial workers, and of that, an increase of 2 million manufacturing workers.

As of 2019, Ukraine had 118,935 manufacturing businesses, some with as few as five workers. Today it is unquestionably far less, but Ukraine should aim to increase that by about 50,000 new manufacturing enterprises by 2032, and expand the size and workforce of existing manufacturing establishments. The leading edge of this should the machine-tooling industry, and master machine tool technicians should be brought in from China, Germany, Italy and Switzerland, to work with Ukrainian machine tool experts to educate a next generation of machine tool workers.

Ukraine has an official youth unemployment rate fluctuating between 15% and 22%, though the real rate is reportedly much higher. Ukraine should establish a Civilian Conservation Corp, modeled upon that which U.S. President Franklin Roosevelt created in the United States in March 1933 to employ and train unemployed youth. The Ukrainian Corps should focus on medical and hospital assistance work, and even supportive positions in building hospitals and other infrastructure, along with educational courses taught in the evening, as part of a World Health System along the lines proposed by Schiller Institute founder Helga Zepp-LaRouche.

Second, Ukraine will have to rebuild many of its cities, and reconstruct and modernize its industrial belt. A significant part of the area’s industry is concentrated in two major regions: the Dnipropetrovsk Region, in the southeastern part of the country, and the DPR, in the east, each of which had produced about 17% of pre-war Ukraine’s industrial output.

The DPR concentrates predominantly on steel production, the chemical industry, and coal mining. It also has science centers. It is important that Donetsk city and Mariupol comprise two ends of a single industrial corridor with industrial enterprises. In Mariupol, the company Metinvest, controlled by the billionaire Rinat Akhmetov, owns two large steel mills, as well as other facilities that together reportedly employ 40,000 people. The DPR has been adversely affected by the fall in coal production. In 2013, Ukraine produced 84 million metric tons of coal. Last year, it was down to 29 million tons, a steep two-thirds drop. Much of the area’s mines are located in the Donbas region. Several of the DPR’s coal mines have been flooded by heavy rains over the last few years, and rendered inoperable, and the central government in Kiev has done little to help. This has damaged Ukraine’s steel production. The British Royals’ holy “Great Reset” crusade against coal is further damaging Ukraine.

The Dnipropetrovsk Region, a center of heavy industry, is dotted with many facilities devoted to producing a wide range of industrial and capital goods, including cast-iron, rolled metal, pipes, machinery, mining machinery, agricultural equipment, tractors, trolleybuses, refrigerators, and food-processing.

Several large mining companies are located in Kryvyi Rih, the longest city in Europe, which is located in the Dnipro Region. ArcelorMittal, the largest steel producer in Ukraine, with between 4 to 6 million tons of annual production, is located in Kryvyi Rih. Yuzhmash and Yuzanoye, two large state-owned companies which were at the heart of the Soviet Union’s defense and space production capability, are also located in the Dnipro Region.

In these two industrial centers, which together produced more than one-third of Ukraine’s industrial output, some of the factory equipment is worn down — some dating from the middle part of the Soviet era — and a portion of the infrastructure is deficient. Their survival will require significant capital investment in the technological upgrade and modernization of capital goods and plant, as well as building many new factories. This should be a joint Marshall Plan-type effort of the industrial nations of the West and the East, not unlike what was required to help rebuild Germany after World War II.

Third, railroads. The attached figure, labeled “Railroad and Road Corridors Across Eurasia,” which first appeared in the Schiller Institute’s “The New Silk Road Becomes the World Land-Bridge” report, Volume II, shows Ukraine’s physical centrality to the World Land-Bridge. Currently, 80-90% of the freight traffic that is transported from Asia to Europe goes through the Northern Corridor rail lines, which traverse Russia, and that has been brought to a near stand-still by the sanctions.

Part of Ukraine’s rail network is aged, and is in great needed of resuscitation. Half of its 21,640 kilometers (13,447 miles) is electrified, but it cannot handle high-speed traffic except in a few sections. However, in 2021, Krzaliznytsia, the Ukrainian Railways, signed an agreement with the Italian Ferrovie Dello Stato Italiane to conduct a pre-feasibility study for the introduction of high-speed rail traffic in Ukraine. At the center of the proposal is construction of a high-speed rail line from Odessa to Kyiv to Lviv, a distance of 790 kilometers (489 miles). This high-speed route should be extended to connect western Ukraine (where Kyiv and Odessa are located) to Dnipro and DPR in the east. The system covers passenger transport, but it should be extended to carry freight as well. The Chinese, the world’s foremost power in rail construction, are also interested in building high-speed rail in Ukraine.

A high-speed rail line to transport passengers and freight through Ukraine would require about 10,000 kilometers (6,200 miles) kilometers of new lines.

Fourth, Ukraine has a very prominent and competent space industry, anchored by the Kyiv-based Antonov Aeronautics, and the Yuzhmash and Yuzhnoye enterprises. Both Yuzhmash and Yuzhnoye are headquartered in the southeastern Ukrainian city of Dnipro, in Dnipropetrovsk Region, dubbed “Rocket City” after its space industry. During the Soviet era, Dnipro served as one of the main centers for space, nuclear and military industries and played a crucial role in the development and manufacture of ballistic missiles for the USSR. One of the most powerful intercontinental ballistic missiles (ICBMs) used during the Cold War was the R-36, which later became the paradigm of the Tsyklon family of launch vehicles. Both the R-36 and the Tsyklon were designed by Yuzhnoye and manufactured by Yuzhmash.

The way out of military production was the space industry. Both enterprises became the spine of the country’s space industry, building over 100 launch vehicles a year. In the West, they gained attention for designing and manufacturing the first stages for the Antares rocket, which launches the Northrop Grumman Cygnus cargo vehicle to the International Space Station. And Yuzhnoye also manufactures engines for Europe’s Vega rockets.

In addition to space vehicles and rockets, Yuzhmash manufactures landing gears, castings, forgings, tractors, tools, and industrial products. These companies and others of Ukraine’s research and manufacturing facilities, possess giant hangars and complex test benches, representing billions of dollars of investment.

Antonov Aeronautics makes especially heavy-lifting military and commercial transport vehicles, as well as passenger airlines, and is also a world leader in moving space components by air and completing cargo-related satellite shipments. In 2016, it was folded into the newly created Ukrainian Aircraft Corporation.

Yuzmash, Yuzhnoye and Antonov employ a combined 40,000 employees, many of whom are engineers, space scientists, etc. They and their complex components, represent a real gem, not only for space exploration, but for their broader capabilities, a portion of which could produce new products such as laser machine tools, and many other advanced machines that Ukraine and other nations will need.

Fifth, Ukraine’s rich black soil is a blessing for mankind. Ukraine is one of the world’s largest grain exporters, exporting, according to the USDA’s March 2022 forecast, for the period 2021/2022, 20 million metric tons of wheat, 27 million metric tons of corn, and 6 million metric tons of barley. It is the world’s largest producer of sunflower seed, and one of the world’s top seven producers of potatoes, dry peas, carrots, cucumbers, pumpkins, cabbage, rapeseed, sugar beets, and so forth. Under the right international arrangements, it could feed a portion of Africa.

Sixth, all of these projects require a tremendous amount of credit. The IMF-City of London-Wall Street-dictated economic policies in Ukraine must be entirely and promptly canceled. They have brought destruction, looting, starvation, and disease upon the Ukrainian people from 1991 through the present.

The credit requirements for the programmatic outline for Ukraine’s reconstruction described above, will total easily one-half to one trillion dollars. That cannot be achieved through IMF-City of London’s speculative casino world monetary system. Ukraine should apply the Glass-Steagall law to put its financial system through immediate bankruptcy reorganization, and establish a Hamiltonian National Bank to replace its central bank, to emit the necessary volumes of directed credit to the productive side of the economy.

All of these measures will be implemented, as we outlined in the opening section of this document, within the context of a new world credit system, which, conjoined to the Belt and Road Initiative, will generate a revolution in world development.

********************

Box 1

LaRouche’s “Four New Laws”

On June 8, 2014, Lyndon LaRouche wrote a document titled “The Four New Laws to Save the U.S.A. Now! Not an Option: An Immediate Necessity,” which emphasized the following four policy requirements:

- The immediate re-enactment of the Glass–Steagall law instituted by U.S. President Franklin D. Roosevelt, without modification, as to principle of action. This means putting the entire speculative financial bubble through bankruptcy reorganization.

- A return to a system of top-down, and thoroughly defined, National Banking, as specified by the U.S. first Treasury Secretary, Alexander Hamilton.

- The purpose of the use of such a Federal credit-system is to generate high-productivity trends in improvements of employment; with the accompanying intention, to increase the physical-economic productivity, and the standard of living, of the persons and households.

- Adopt a fusion-driver ‘crash program’ to promote the fundamental breakthroughs in science which unlimited economic growth and development require.

********************

Box 2

LaRouche on Tariffs and Trade

The following excerpt is taken from Lyndon LaRouche’s January 12, 2004 essay, “On the Subject of Tariffs and Trade.“

Now, the world’s present, floating-exchange-rate monetary-financial system is hopelessly bankrupt. It must be placed into governments-controlled receivership for necessary forms of administration and reorganization. Virtually none of the leading banking institutions of western Europe and the Americas (among other cases) are not implicitly bankrupt presently. Therefore, the first, most immediate objective of intervention by sovereign governments must be stability of the normal functions of society; the second, short- to medium-term objective, must be an increase in productive employment to levels sufficient to bring current accounts of nations into balance; the third objective must be the negotiation of a nested array of long-term sets of protectionist treaty-agreements on credit, tariffs, and trade among a set of leading nations. The latter agreements should range from one to two generations: corresponding to capital cycles of from twenty-five to fifty years.

The possibility of a recovery from the condition presently bequeathed to us by the combination of the floating-exchange-rate IMF system and the wildly aberrant behavior of central banking systems of nations, depends upon a massive supplement of long-term credit for capital formation, with initial emphasis on capital formation in basic economic infrastructure. To sustain such a program of expansion over two generations, as we must, requires a system in which fundamental borrowing costs must be no higher than between 1-2% simple-interest rates. This can be achieved only under conditions defined by a fixed-exchange-rate monetary-financial system. Therefore, this means a `gold reserve system,’ but not a revival of a British-style (or looney Ezra Pound’s) `honest money’ sort of gold standard system. This also means a system of long-term trade and tariff agreements among nations, to an effect consistent with such goals as long-term growth of capital formation.